As the weather cools and we start to reach for our umbrellas, the focus on the local economic front is the May 9 Federal Budget.

The March quarter CPI, our main measure of inflation, rose 0.5 per cent. This took the annual rate of inflation to 2.1 per cent, the first time it’s been within the Reserve Bank’s 2-3 per cent target band in over two years, reducing the need for further rate cuts to stimulate the economy.

On the global front, the economic spotlight in April shifted to Europe, with France and the UK facing elections that will shape Europe’s economic future. In the UK, Prime Minister Theresa May called a snap general election for June 8 to win a clear mandate for the long process of leaving the European Union.

In France, centrist Emmanuel Macron and far right Marine Le Pen won the first round of the French Presidential elections. Macron, a former economics minister and investment banker is front runner to win the second round of voting on May 7. Investors reacted positively, with the Euro and French stocks rising as did Wall Street. Macron is a free trade supporter with a platform of cutting corporate tax and economic stimulus; Le Pen campaigned on removing France from the European Union. As France is the second biggest member of the EU after Germany, it’s exit would have greater ramifications for the European economy than Brexit, with some economists saying it could spell the end of the Eurozone and push Europe into recession.

Having a good credit score can help you secure the best financial deals, but first you need to understand what your credit score is and what steps you can take to improve it.

Your credit score is based on information collected by credit reporting agencies and documented in your personal credit report. This information includes personal details such as your age and where you live, how much you’ve borrowed and who from, the number of credit applications you’ve made and any unpaid or overdue payments. These could relate to a bank loan, rent, mortgage or even an overdue phone bill. Lenders and credit providers such as banks and credit unions use this information to work out how risky it is to lend you money.

The good news is that you can get a copy of your credit file once a year for free as well as your credit score from online sites such as Creditsavvy, Equifax (previously called Veda) and Finder (which uses Equifax scores).

Depending on the credit reporting agency, you will receive a number out of 1000 or 1200 that’s broken down into five categories, from excellent to below average. If you fall into one of the lower categories, lenders may ask for more information or deny you credit.

It’s worth checking your credit file before you apply for a loan to make sure the information is accurate and that you haven’t been the victim of fraud or identity theft. If there are mistakes, credit providers and reporting agencies are legally obliged to investigate and correct them free of charge.

You can increase your chances of being approved for a loan by understanding your score, correcting any errors and improving your creditworthiness with some simple actions.

If you are about to start house-hunting or see an attractive investment, then timely access to credit is critical. Knowing your credit score and improving it if necessary can not only speed up your

If you would like to discuss ways to tackle debt and get your finances in shape, give us a call.

That sounds like a lot, until you start writing it all do

If you think the above mentioned costs sound like a lot, consider what some people spend on treats, accessories and ‘experiences’ for their furry pals. A world apart from basic kennels, luxury ‘pet hotels’ offer pampered pooches and felines exclusive suites with full sized beds, swimming pools, spa treatments and regular Skype calls with the owner – for up to $100 per day. The rise of designer pet boutiques like Dogue says something about the way pets have shifted from working animals to fashion accessories. At these high-end stores, you can pick up a dapper bowtie for $60, designer bed for $180, high tech raincoat for $150, or Swarovski crystal collar for $70.

While it’s possible to forego the luxury treats, keeping your pets in good health is an essential, but sometimes significant, expense. Many cat, dog and bird breeds have common health problems that can crop up sooner than expected, and get worse as the animal ages. These include breathing disorders, joint disease, and even cancer. These problems may require surgery or medical intervention that can cost several thousand dollars to resolve. A hip replacement can cost $6,000. Canine cancer treatment may cost $10,000-$20,000, once diagnostics, surgery, chemotherapy and follow-up care are factored in.ii

Growing uptake rates show Aussies are increasingly using pet insurance to mitigate unexpected vet bills.iii Insurance is available for accidents only, accidents and illness, or all vet bills including routine care. The monthly premium can vary depending on variables like breed and age. If you decide that you don’t want to take up insurance it’s important to make sure that you can manage to cover unforeseen medical emergencies.

All in all, any loving pet owner would agree – having a pet is well worth the cost. They can provide endless entertainment, companionship for older people, life lessons in caring for kids, a great reason to exercise, and unconditional love. We all want to give our furry friends a full life and budgeting for both the ongoing and unexpected costs can ease the strain.

i https://www.moneysmart.gov.au/life-events-and-you/life-events/getting-a-pet/the-cost-of-a-pet

ii http://www.smh.com.au/environment/animals/top-treatment-for-pet-patients-20120913-25uwe.html

iii http://www.ibisworld.com.au/industry/default.aspx?indid=623

![]()

![]()

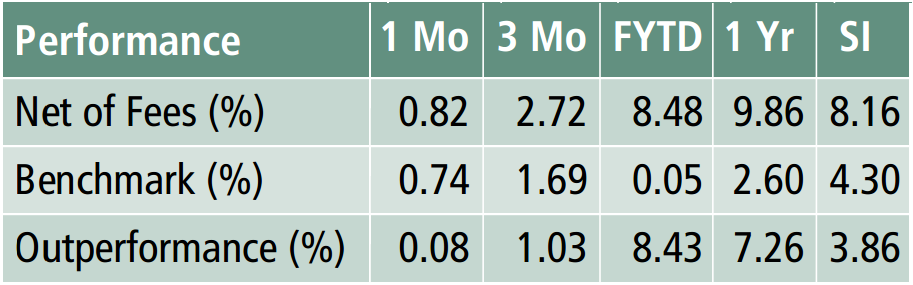

The PIMCO Income fund is a portfolio that is actively managed and invests in a broad range of fixed income securities to maximise current income while maintaining a relatively low risk profile, with a secondary goal of capital appreciation. The fund taps into multiple areas of the global bond market, and employs PIMCO’s vast analytical capabilities and sector expertise to help temper the risks of high income investing.

*Fund performance as at 31st April 2017

** The benchmark is the Bloomberg Barclays Global Aggregate Index (AUD Hedged)

The aim of the fund is to provide a competitive and consistent level of income without compromising total return, and has also been designed to provide liquidity when needed. The fund achieves this through its multi-sector approach which allows it to seek out the best income-generating ideas in any market climate, targeting multiple sources of income from a global opportunity set.

PIMCO expects global growth to remain positive in 2017, especially in the U.S. However, there will be substantial differences in growth dynamics among countries. They remain focused on diversification and staying senior in the capital structure as the U.S. economic recovery continues. In this environment, the Fund will seek to pay a consistent distribution while potentially generating capital appreciation and principal protection by focusing on the best opportunities around the globe.

As U.S. interest rates recalibrate higher, the Fund will seek to balance exposures to high-quality duration to protect against downside risk over the cyclical horizon. Australian duration remains an attractive hedge to risk assets. In addition, we are focused on allocating to securities with floating interest rates as a way to reduce sensitivity to interest rate volatility and protect principal as interest rates rise.

Please note this information is of a general nature only and has been provided without taking account of your objectives, financial situation or needs. Because of this, we recommend you consider, with or without the assistance of a financial advisor, whether the information is appropriate in light of your particular needs and circumstances.

Copyright in the information contained in this site subsists under the Copyright Act 1968 (Cth) and, through international treaties, the laws of many other countries. It is owned by EFDB Pty Ltd unless otherwise stated. All rights reserved. You may download a single copy of this document and, where necessary for its use as a reference, make a single hard copy. Except as permitted under the Copyright Act 1968 (Cth) or other applicable laws, no part of this publication may be otherwise reproduced, adapted, performed in public or transmitted in any form by any process without the specific written consent of EFDB Pty Ltd.

EFDB Pty Ltd | Sydney CBD | Northern Beaches | ABN 64 112 871 922 | AFSL 311720

© 2025 EFDB Pty Ltd trading as Diamond Blue Financial Services, ABN 64 112 871 922, AFSL 311720. SiteSuite Websites